In today’s competitive business environment, organizations must manage cash flow efficiently, assess financial performance accurately, and control credit-related risks to remain profitable. Failure to strengthen financial analysis and credit management systems often leads to delayed payments and rising bad debts. On the flip side, companies that invest in these areas gain stronger liquidity and sustainable growth opportunities. Therefore, proactive financial management allows organizations to identify risks early, maintain healthy customer relationships, and protect long-term profitability.

Why Financial Analysis and Planning Matter

Financial analysis and planning are the foundation of a successful business strategy. Without understanding financial performance, organizations cannot make informed decisions about investments, operational expenses, or growth. Financial analysis evaluates profitability, liquidity, efficiency, and stability, enabling managers to identify trends affecting business sustainability by analyzing cash flow statements, balance sheets, and income statements. Accurate financial forecasting prepares organizations for market uncertainties and effective resource allocation.

Additionally, financial planning supports strategic decision-making through realistic budgets, performance targets, and investment priorities. Consistent monitoring of financial indicators allows businesses to respond faster to economic changes and avoid strain. As a result, sound financial planning strengthens business resilience, positioning companies to manage debt, maintain operations, and pursue expansion without excessive risk.

The Growing Importance of Credit Management and Accounts Receivable

Collecting payments on time is as critical as generating revenue. Many businesses face financial pressure due to delayed customer payments, leading to cash flow shortages and increased borrowing costs. Credit management involves assessing customer creditworthiness, setting credit limits, and monitoring payment behavior. Effective credit policies minimize exposure to high-risk customers while maintaining healthy relationships.

Accounts receivable management focuses on tracking outstanding invoices and ensuring timely collections. Actively monitoring receivables helps identify overdue accounts early and take corrective action. Efficient receivables management improves working capital availability, allowing businesses to reinvest funds without heavy reliance on external financing. Thus, neglecting credit control can lead to increased bad debt, reduced cash flow stability, higher operational costs, damaged supplier relationships, and lower profitability.

Common Challenges in Debt Collection and Credit Control

Debt collection is a difficult aspect of financial management. Poor follow-up procedures weaken recovery efforts and increase financial losses. Inconsistent credit approval processes, where credit is extended without proper financial assessments, increase the likelihood of defaults. Delayed invoice processing, often due to errors or late delivery, inevitably leads to payment delays. Ineffective communication between finance teams and clients can worsen collection difficulties, as businesses may hesitate to pursue overdue accounts aggressively for fear of damaging relationships.

However, inconsistent enforcement of payment terms encourages chronic late payments, which weakens credit discipline. Technology gaps also contribute to inefficient debt management, with manual tracking systems struggling to monitor aging accounts accurately. Economic uncertainty, including inflation and market disruptions, frequently increases the risk of delayed payments and loan defaults. Therefore, companies must implement structured credit control systems supported by clear policies, automation tools, and skilled personnel.

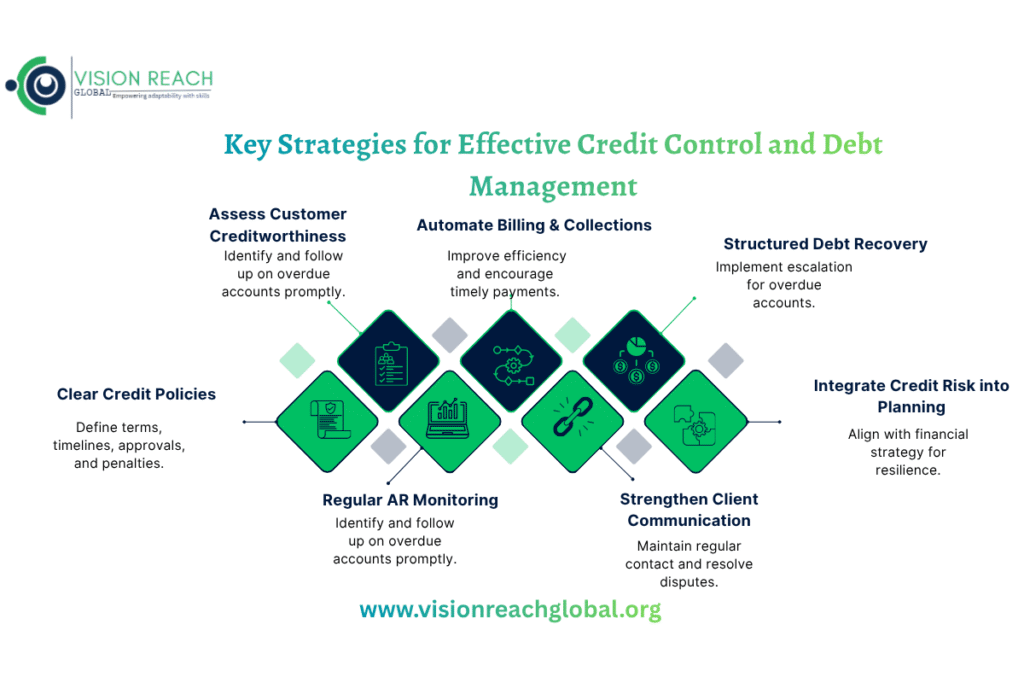

Key Strategies for Effective Credit Control and Debt Management

Businesses can significantly improve financial stability through proactive credit control and debt management strategies. These measures reduce financial risk, enhance operational efficiency, and increase customer accountability.

- Establish Clear Credit Policies: Define credit terms, payment timelines, approval procedures, and penalties for overdue accounts. Transparent policies ensure consistency and reduce disputes.

- Conduct Customer Credit Assessments: Evaluate customer financial history, repayment capacity, and risk exposure before extending credit to avoid high-risk transactions.

- Monitor Accounts Receivable Regularly: Continuous monitoring helps identify overdue accounts early and initiate timely follow-ups. Aging analysis reports prioritize collection efforts based on risk.

- Automate Billing and Collection Processes: Digital systems improve invoice accuracy, payment tracking, and reporting efficiency. Automated reminders encourage timely payments.

- Strengthen Communication with Clients: Professional and consistent communication improves debt recovery. Maintain regular contact regarding payment obligations and resolve disputes promptly.

- Develop Structured Debt Recovery Procedures: Implement escalation protocols for overdue accounts, including reminders, negotiations, and legal recovery processes when necessary.

- Integrate Credit Risk into Financial Planning: Align credit management with broader financial planning and enterprise risk management strategies to forecast potential losses and maintain financial resilience.

Case Snapshot

A mid-sized distribution company faced severe cash flow problems despite strong sales growth. A review revealed that over 40% of outstanding invoices were over 90 days overdue, due to a lack of formal credit approval procedures and manual receivables tracking. Collection follow-ups were inconsistent, allowing debts to accumulate.

Thereafter, the company implemented automated accounts receivable software, revised credit policies, and introduced structured debt collection procedures. Within twelve months, overdue receivables decreased substantially, cash flow improved, and operational efficiency increased. This demonstrates how effective financial analysis and credit management can transform business performance.

Conclusion

In a nutshell, financial analysis, credit management, accounts receivable control, and debt management are essential for sustainable financial performance and organizational stability. Strengthening financial planning and enforcing disciplined credit control measures improves liquidity, reduces bad debt, and supports long-term growth. Proactive debt recovery strategies position businesses to navigate economic uncertainty with greater confidence. Companies prioritizing strong financial management practices will build healthier cash flow systems, stronger customer accountability, and a greater competitive advantage.

Call to Action

Organizations seeking to strengthen financial performance should invest in professional training and advisory services focused on:

- Financial Analysis and Planning

- Credit Management, Debt Collection, and Accounts Receivable Optimization

- Debt Collection Strategies

- Credit Control and Debt Management Systems

Equipping finance teams with these capabilities can significantly improve operational efficiency, reduce financial risk, and support sustainable business growth.